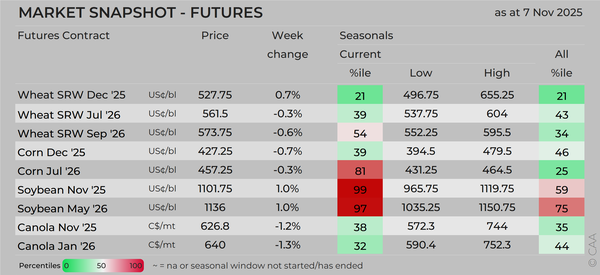

MARKETS:

Monday Check-in

A week of calibration for crop estimates and price competitiveness.

Summary

- The USDA updates its crop estimates after two months, testing the market’s conjectures in that time.

- US soybean prices likely still have some more adjustment to get back to competitive levels.

- Wheat might finally be trading as a momentum-free market, making range trading more likely.

- And the US Dollar has been creeping higher, making it a potential factor for all prices.

Grain and oilseed markets are set for a week of calibrations. The USDA will publish updated production estimates for the first time since September. The soybean market is looking to find a level where China is a buyer. Wheat prices might, at last, have killed the weak momentum that had, self-fulfillingly, prevented a season low for prices. And, the US Dollar’s creep higher might have a role to play. The markets overall lack any major weather issues to drive prices substantially higher.

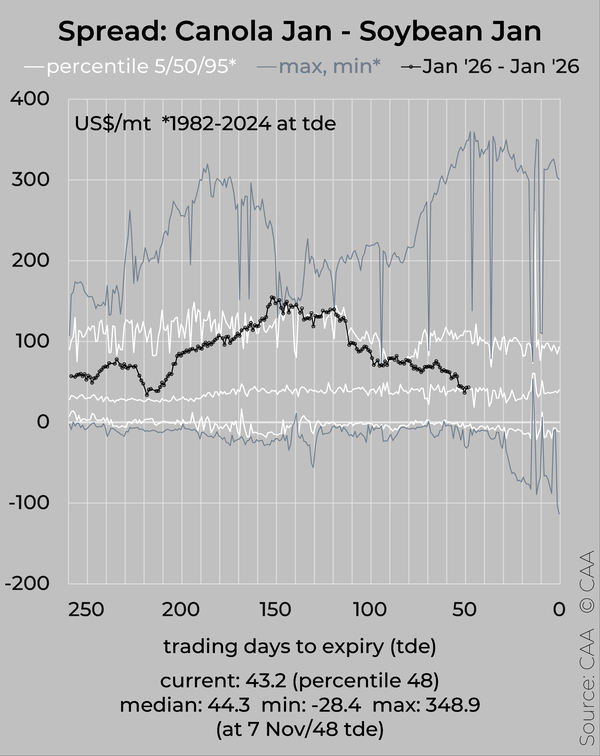

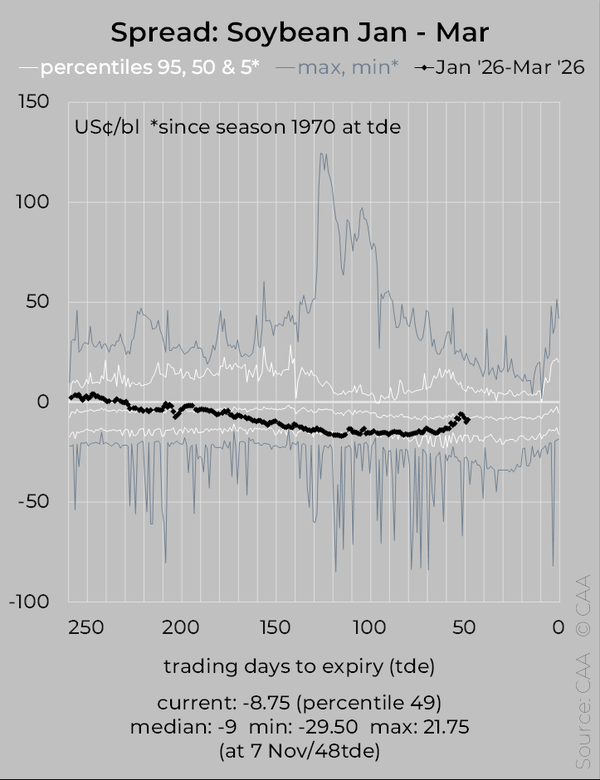

UNSCRAMBLING SOYBEANS

The jump in US soybean prices after the China-US trade truce seems to have been a step too far. Prices reached levels that seemed to presume there was a captive buyer. As it turns out, China’s importers were not going to buy at any price. Moreover, the market did not seem positioned for the trade truce’s terms. Understandable, given the uncertainty. The resulting scramble, though, left US prices at uncompetitive levels at times. And it left markets misshapen. Canola prices pretty much ignored the soybean price moves (see lhs chart below). Soybean calendar spreads sprang to levels that suggested that there was very little US supply pressure (rhs chart below). Prices retreated towards the end of the week, but likely still have to fall further to reach competitive levels.

WEAK WHEAT MOMENTUM ENDS?

Wheat prices also enjoyed a rally last week. China buying some US wheat certainly helped the mood. We also suspect that investors, heavily short for much of this season, continued to exit that position, adding a bid. Some of the price gains were relinquished by week’s end. However, the rally might have ‘snapped the stick’ of negative momentum.

US wheat prices’ negative momentum has been (self-fulfilling) headwind for most of this season. Most momentum indicators will now have swung to neutral. Some very long-cycle metrics remain negative, but they are unlikely to drive many large-volume momentum strategies. The momentum swing likely triggered a broad exit by momentum investors. That buying likely pushed up prices, prompting other players to do the same. We expect CoT reports, when they resume, to show that investors’ short positions in SRW and HRW wheat are much smaller.

Wheat’s evolution from here, therefore, starts with a neutral directional bias and cleaner positioning. We think it is unlikely the gains to date presage an extended rally. The supply context is neutral or better into 2026. The USDA’s update this week likely confirms that context, especially for the US. And rubber stamps the market’s bigger crop forecasts for Argentina and Australia. The market also lacks any influential weather worries. The context suggests wheat prices are likely to start a period that establishes a range. Prices will fluctuate as it searches for a point that keeps wheat flowing from major exporters. US wheat exports have, if export inspections are any guide, been healthy. More US export sales to China would be a bonus.

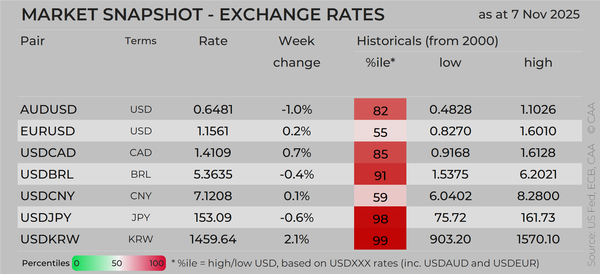

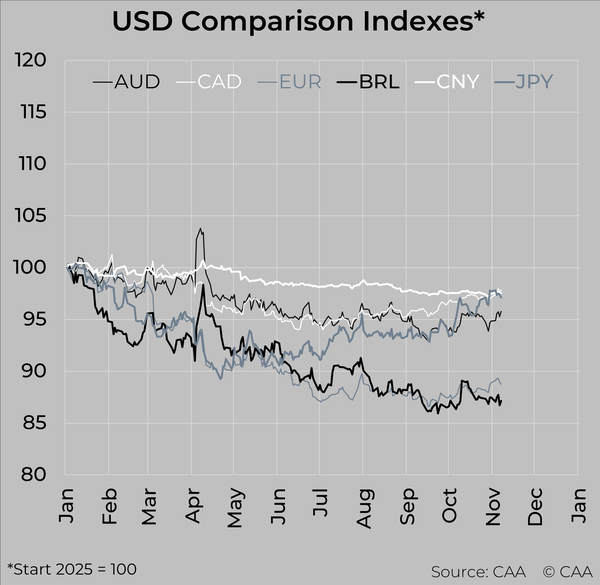

IS GREENBACK SNEAKING HIGHER?

The US Dollar has been gravitating higher since about mid-September – with one exception, China’s Yuan (CNY). China’s central bank seems to have leant against any CNY fall. The gains are modest: the greenback remains below where it started 2025. The gains are a break from the broadly flat trend since mid-year. And, importantly, the micro-trend has persisted through changing views about US monetary policy. The gains so far have likely not been a noticeable drag on US$ prices. Other influences have been much more important. Further greenback gains, though, might have a greater impact as other influences recede. And the influence would amplify if the US’ export pace falters. The soybean price impact is likely to be modest. The USD’s most modest gains have come against Brazil’s Real and is all but ‘unch’ on the CNY.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}